The basic rule is simple: save 20% of your income. And honestly, there's nothing wrong with that…if you're starting from zero, "20%" is a perfectly fine number to aim for. We wrote a whole post on the 50/30/20 rule explaining why it works for most people most of the time.

But once you're past the beginner stage, that percentage stops being useful. Because 20% of your income has no idea what your rent is. It doesn't know you have a wedding to pay for in two years. And it can't tell you that your car insurance is going to land in March like a brick through the window.

The Quick Answer

Ask yourself two questions.

- How much can I save? (what's left after your real expenses including the yearly stuff most people forget).

- How much do I need to save? (your goal, divided by how many months until you want to hit it).

The bigger of those two numbers is your monthly savings target. If they don't match, something has to give: the timeline, the goal, or an expense. That's the whole article in three sentences. The rest is just how to answer both questions honestly.

The two-formula method (this is the whole trick)

The 20% rule asks one question: what should I save? And it gives you one number, with zero context.

The advanced method asks two. Then it runs two formulas and makes them argue with each other.

- Formula 1 — What you CAN save: Income − (Monthly Expenses + Yearly Expenses ÷ 12) − Buffer

- Formula 2 — What you NEED to save: Goal Amount ÷ Months Until Goal

You compare the two. The bigger number wins. If your budget can't fund your goal, something gives: the deadline, the goal size, or how much you're spending elsewhere. Savings isn't a percentage. It's a negotiation between your wallet and your wishlist.

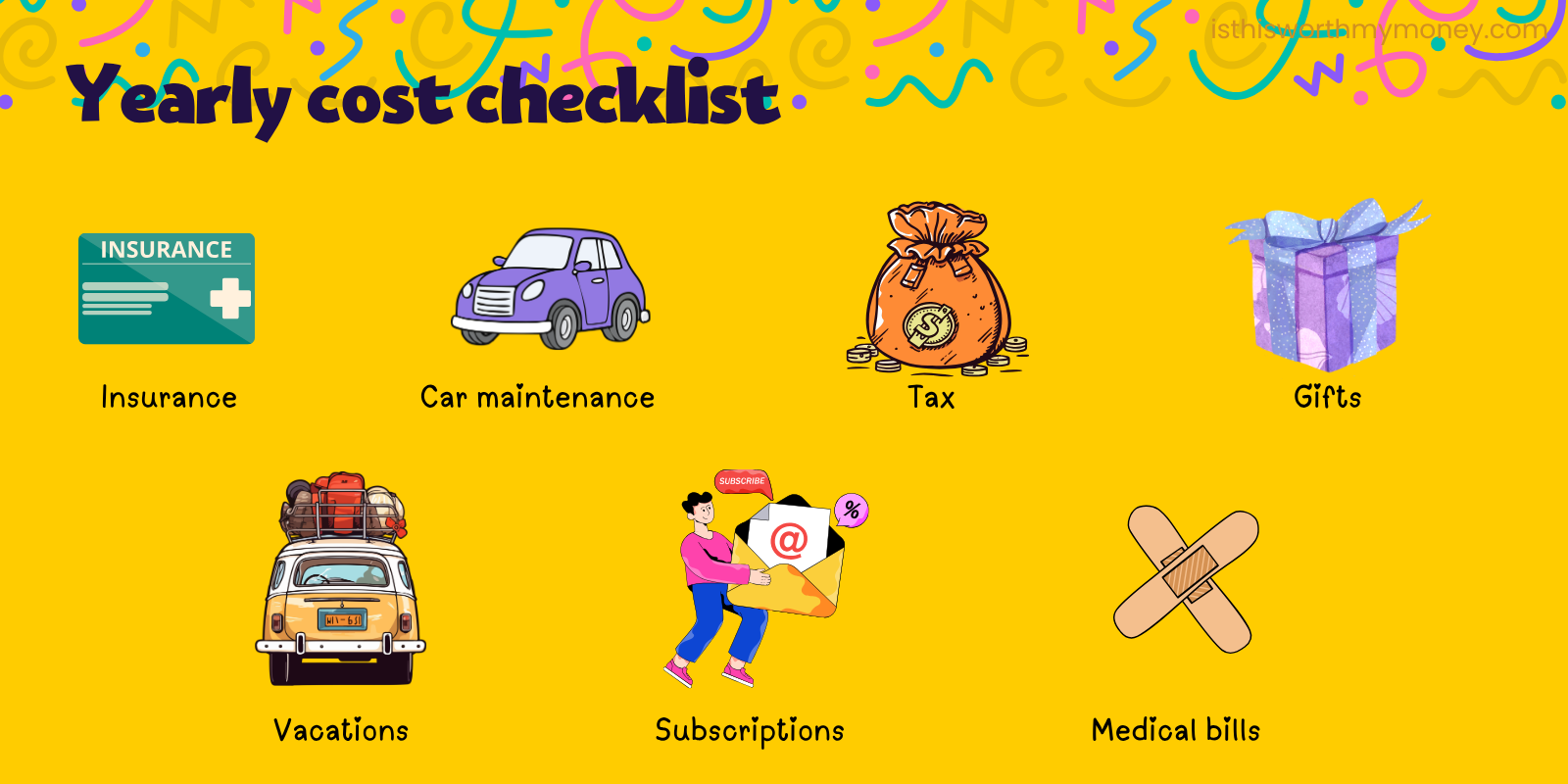

The yearly expenses that quietly break your budget

You tracked your monthly expenses. Rent, food, transport, subscriptions. Felt great about yourself. Then March showed up with a $1,200 car insurance bill and the whole plan exploded.

This is the trap most budgets fall into. They count the bills that show up every month and forget the ones that ambush you once or twice a year. Insurance premiums. Think annual subscriptions, holiday gifts, that one trip, car maintenance that always costs more than you expected, and so on.

These aren't optional expenses. They're just hidden expenses. And they're the difference between a budget that works on paper and a budget that survives an actual year.

The fix is one line: every yearly bill ÷ 12 → add to your monthly number.

Quick example: A $1,200 insurance premium is $100/month. $800 in holiday gifts is $67/month. A $1,500 trip you take every summer is $125/month. That's almost $300/month you weren't tracking, which is more than most people's grocery bill.

Now your "monthly expenses" actually reflect what a month costs you on average. No more ambushes.

If you want to see what this looks like in practice, check out our budget breakdown for a remote worker, every category is accounted for, including the yearly stuff.

The "did you forget this?" checklist

Run through this list. If any of these aren't in your monthly math, add them now (yearly cost ÷ 12):

Most people find at least three things they hadn't counted. Add them all up, divide by 12, and that's the number your old budget was missing.

Saving without a goal is a slow leak

Here's the honest reason most "savings" eventually disappears: it didn't have a name.

When money sits in an account labeled "savings," your future self will find a reason to spend it. The justifications come easy because the money has no address, it's just "savings," available for whatever feels important right now.

The fix: every dollar you save needs a destination. Three buckets, three different monthly numbers. Pick the one that's most urgent and start there.

- Emergency fund. Three to six months of expenses, sitting in a separate account. This goes first. It's the only fund that protects the other two. Without it, one bad month wipes out everything else you saved. (Fidelity recommends 3–6 months of essential expenses, and that's the standard most planners stick to.)

- A specific goal. Wedding, trip, car, down payment, gadget. Divide the goal by months until you need it.

- Future you. 10–15% of gross income, ongoing, automated, and forgotten. This is the retirement bucket. You don't think about it. It just happens.

Once you've got your buckets named, our guide on how to save money with 11 weird tricks covers the tactical side, actually freeing up the cash to fill them.

Now make the two numbers meet

Here's where it gets interesting. You've got two numbers, what you CAN save and what you NEED to save. Now you put them side by side and see what happens.

If they match, great. Set up an automatic transfer for that amount on payday and stop thinking about it. If they don't match, that's actually useful. The gap tells you exactly what to fix.

Rather than working it out on paper, plug your numbers into the calculator below.

Want more tools? Our roundup of the best free budget calculators in 2026 covers alternatives if you want a second opinion on the math.

When the math says "impossible" - read this before giving up

If your two numbers don't meet and the gap looks huge, you're not failing. You're doing the math most people skip.

Most "I can't save enough" moments are actually a sign you ran the formulas correctly. The number just isn't the one you wanted. That's fine. There are three levers, and you only need to pull one.

Lever 1: Stretch the timeline. This is the lever that works most often. "$10K in 12 months" is brutal. "$10K in 24 months" is obvious. Same goal, totally different stress level. If your deadline is artificial (and most deadlines are), extending it costs you almost nothing.

Lever 2: Cut one category, not all of them. A subscription audit or a commute change beats a guilt-driven "everything-cut" budget that lasts a week. Look at your spending and find the one category where $50 disappears without giving you joy. Cut that. Leave the rest alone.

Lever 3: Shrink the goal. A $7,000 emergency fund still saves you. The "perfect" $10,000 number isn't the only correct one. A smaller goal you actually hit beats a bigger one you give up on in two months.

The one mistake worse than saving too little is not saving anything because the "right" number felt out of reach. $50/month for a year is $600 in a savings account. Zero is zero. The math on that one isn't complicated.

The Verdict

There's no universal "right" amount to save per month. There's only what your income, your real expenses (including the yearly stuff), and your goal actually allow.

If you want a number to start with: aim for 15–20% of your take-home pay. But check it against your real budget and your real goal before you commit. A 10% saver with a clear emergency fund target will beat a 20% saver who's saving toward nothing, every single time.

The formula matters more than the percentage.

So run your numbers through the calculator. Write down the target. Set up an automatic transfer for that exact amount on payday. The automation is the part most people skip, and it's the part that decides whether the plan actually works.

The Latte Factor - How Small Daily Purchases Add Up.