Every budgeting guide eventually throws a bunch of categories at you. Groceries, utilities, subscriptions, gas, insurance, "miscellaneous." By the time you're done sorting, you've lost the will to budget at all.

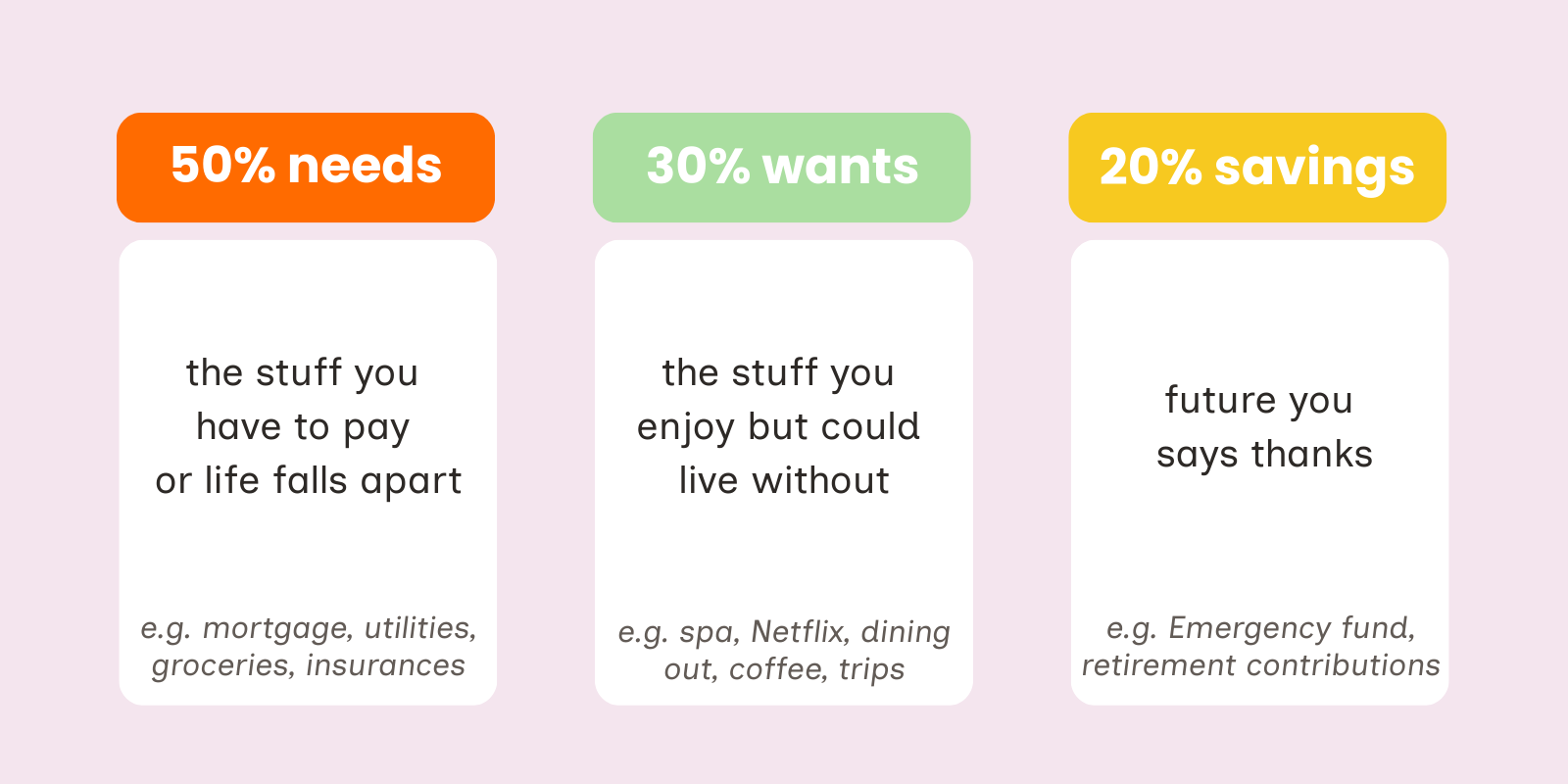

The 50/30/20 rule skips all of that. It only has three categories. That's it. Three.

The idea in 10 seconds

Take your monthly income after tax and split it like this:

The concept was popularized by Senator Elizabeth Warren in her book All Your Worth. It's stuck around because it's dead simple and works for most people without requiring a spreadsheet or an accounting degree.

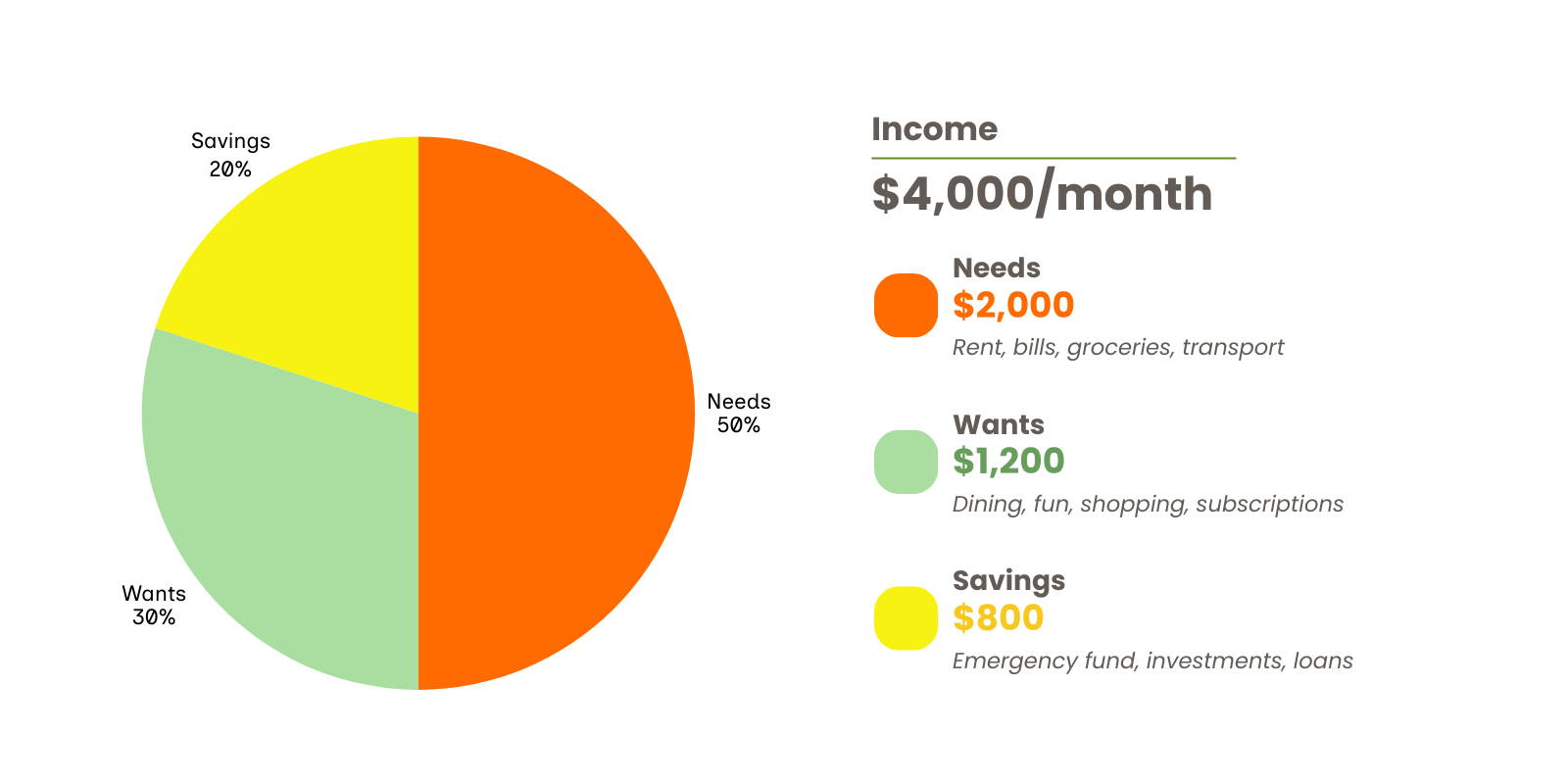

What it actually looks like

Let's say you take home $4,000/month after tax. Here's how the split works:

That's the whole system. No 47 subcategories. No color-coded spreadsheet. Just three buckets.

The part that trips people up: needs vs. wants

This is where most people get it wrong, and it's honestly the only hard part.

A need is something that would cause real problems if you stopped paying for it. Rent. Electricity. Basic groceries. Health insurance. The minimum payment on your credit card.

A want is everything else. Even things that feel essential.

Here are a few that catch people off guard:

| You might think it's a need | It's actually a want |

|---|---|

| A car | Maybe. But the brand-new SUV is a want. A reliable used car to get to work is the need. |

| A phone plan | Yes, but the $100/month unlimited plan is a want. A basic plan covers the need. |

| Groceries | The food is a need. The $8 organic cold-pressed juice is a want. |

| Internet | Basic internet for work is a need. The fastest tier with streaming bundle is a want. |

There's no shame in spending on wants. That's literally what the 30% is for. The goal is just to put things in the right bucket so you're being honest with yourself about where your money goes.

"My rent alone is 40%. Now what?"

Yeah. If you live in a city like New York, San Francisco, or really any major metro area, 50% for all needs might not be realistic. That's fine. The rule is a starting point, not a law.

Here are a few common adjustments:

- 60/20/20 - Your cost of living is high but you still want to save something meaningful.

- 50/25/25 - You're focused on crushing debt fast and willing to cut back on wants.

- 70/20/10 - Money is tight right now. You're covering essentials, keeping a little for yourself, and saving what you can. That still counts.

The percentages matter less than the habit. If you're splitting your income into these three buckets at all, you're ahead of most people.

A real scenario

Meet Alex. Takes home $3,500/month after tax. Lives in a mid-sized city.

Here's what Alex's month looks like using 50/30/20:

Needs (50% = $1,750)

- Rent: $1,100

- Utilities: $150

- Groceries: $300

- Car insurance + gas: $200

Wants (30% = $1,050)

- Dining out: $250

- Subscriptions (Spotify, Netflix, gym): $75

- Shopping/clothes: $150

- Weekend activities: $200

- Leftover cushion: $375

Savings & debt (20% = $700)

- Emergency fund: $300

- Student loan extra payment: $200

- Retirement contribution: $200

Alex's needs come in right at $1,750. Wants leave some breathing room. And $700/month toward savings and debt means $8,400 a year going toward financial goals.

Not life-changing overnight, but after a couple of years? That's a real emergency fund, real progress on loans, and real retirement savings building up.

Try it with your own numbers

The fastest way to see where you stand is to plug your actual income and spending into our monthly budget calculator. It'll show you your current split and how it compares to the 50/30/20 framework.

You might find you're already close. Or you might find your "needs" are eating 70% of your income and there's barely anything left. Either way, seeing the actual numbers is the first step to doing something about it.

Best free budget calculators in 2026 - tools that use the 50/30/20 rule and other methods.